The term “hybrid company” is used to describe a company that is limited both by shares and by guarantee so has two classes of members: Shareholders and Guarantee Members. The former are familiar and well understood the latter less so, although many sporting clubs and societies are structured as companies limited by guarantee and joining members become Guarantee Members.

A Guarantee Member is elected into membership of the company by the directors on condition that the member undertakes to contribute to the debts of the company up to a certain specified maximum amount - typically a relatively nominal amount. As such a Guarantee Member holds a contingent liability, which is an obligation, and this contrasts with the position of the shareholder who holds an asset - the shares.

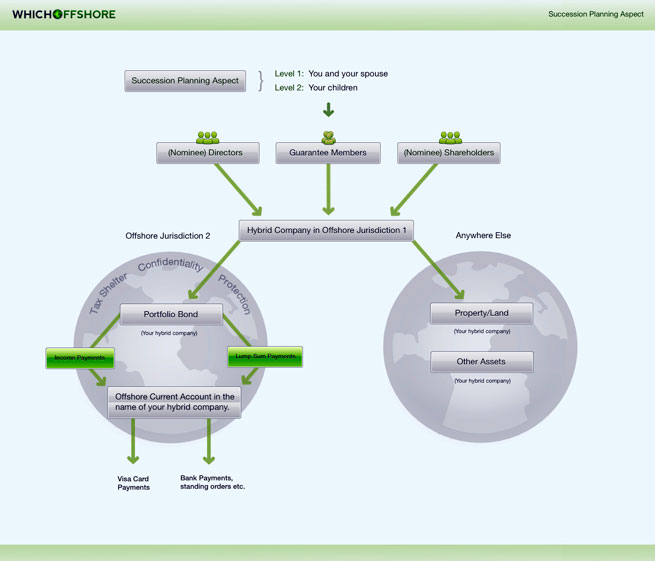

The rights and obligations that attach to each class of membership can be laid down in the Articles of Association of the company or by the directors in board meetings, thereby keeping the terms and conditions of membership confidential. The arrangements that can be made are as infinite and flexible as the different rights and obligations which attach to each class of membership. These can be arranged to suit; and skilful drafting can be used to create structures which are precisely tailored to the different needs of the client. Please see below for a graphical illustration of how a Hybrid Company is structured:

Hybrid companies are often used as quasi-trusts, particularly by persons resident in civil law countries that do not recognise trusts. Typically the company will be structured so that the shares are issued on terms that each carries one vote but no rights to dividends or to participate in the capital or income of the company in any other way. The Guarantee Memberships would be issued on terms that they carry no rights to vote but all the rights to participate in the income and capital of the company. Thus all control rests with the shareholders but all benefits flow to the Guarantee Members. The shares can be issued to professional managers, who therefore act as quasi trustees, but unlike normal shareholders they cannot receive financial benefit from holding the shares. All financial benefits flow to the Guarantee Members who are therefore in a position not unlike the beneficiaries of a classical trust structure. Also a Guarantee Members interest is extinguished on death, when all Guarantee Members have passed away benefits pass to the second tier members (typically your children) so there are no succession problems, no need to obtain probate and so there will normally be no inheritance tax implications or estate duty.

The anti-avoidance legislation enacted by many onshore countries aims to tax the undistributed or untaxed profits of low tax paying companies as though those profits have been received by the shareholders. The different legislations achieve this in different ways but normally focus on the percentage of shares held or the control of the company if control is achieved otherwise than through the ownership of shares. Under the arrangements outlined above the Guarantee Members would not own shares nor have control - as professional managers act as shareholders - so it may be that this type of anti-avoidance legislation is ineffective in taxing profits rolled up within a hybrid structure. Additionally, it will normally be the case that such a structure does not bring about any reporting requirement for the Guarantee Members so, on a practical level, unwanted attention from onshore revenue authorities is avoided.

This is a complex area of offshore estate planning and should be discussed thoroughly with a specialist financial adviser.